What Medicare Part B Covers

If you’re wondering what Medicare Part B covers, you’ll likely be looking for specific outpatient medical expense coverage details.

This insurance part could potentially assist with some of the costs that might be associated with healthcare provider visits, preventive care, and necessary medical equipment. This article will dive into to help you navigate your benefits confidently.

Key Takeaways

- Medicare Part B will likely cover outpatient care, preventive services, and durable medical equipment, and may focus on items and services outside of a hospital setting such as doctor’s visits, diagnostic tests, vaccines, and medical supplies like wheelchairs or walkers.

- Beyond general medical and preventive services, Medicare Part B may also cover medically necessary services, specific home health services, and outpatient mental health care, with a potential emphasis on services that may be in line with accepted standards of medical practice.

- Medicare Part B will likely require payment of monthly premiums, annual deductibles, and coinsurance, with some costs varying by policy and income level; it may not cover cosmetic surgery or routine eye exams unless medically necessary, and could potentially be supplemented with Medicare Advantage or Medigap policies.

Compare Plans in One Step!

Enter Zip Code

Overview of Medicare Part B

Medicare Part B, also known as Medical Insurance, is an integral part of the Original Medicare plan. It will likely cover outpatient care, including necessary services, preventive care, and durable medical equipment.

You could potentially think of it as your safety net when you visit the doctor or need medical services outside the hospital.

Medical Insurance

The cornerstone of Medicare Part B is its comprehensive Medical Insurance coverage. This could cover a wide array of outpatient care such as:

- visits to a healthcare provider, whether for routine check-ups or specialist consultations

- coverage for essential lab tests from urinalysis to blood tests

- other important diagnostic screenings like CT scans, MRIs, and X-rays

In essence, Medicare Part B could provide coverage for a majority of your healthcare needs outside a hospital setting, as Medicare could cover various services and supplies.

Preventive Services

Prevention is better than cure, and Medicare Part B recognizes this. It might cover a variety of preventive services such as vaccinations, screenings, and even annual wellness visits. Some of these services will likely be designed to keep you healthy and catch potential health issues before they become serious problems.

Durable Medical Equipment

Medicare Part B may also cover durable medical equipment (DME). If you need medically necessary equipment like:

- wheelchairs

- walkers

- hospital beds

- oxygen equipment

- prosthetic devices

- orthotics

- mobility scooters

Medicare Part B will likely be able to cover them. As long as the equipment meets the coverage criteria, it might be covered regardless of the brand or type.

Consider it as your reliable medical equipment resource, which could allow you to have the necessary tools for your health journey.

Possible Services Covered by Medicare Part B

Having provided an overview of Medicare Part B’s broad coverage, this article will now examine its potential services more closely.

Whether it’s medically necessary services, home health services, or mental health care, Medicare Part B will likely have it covered.

Medically Necessary Services

When you’re faced with a medical condition and need immediate treatment or diagnosis, you’ll likely need medically necessary services. These services, which will likely be covered by Medicare Part B, include:

- visits to a healthcare provider

- durable medical equipment

- mental health services

- outpatient surgeries

- laboratory tests

- X-rays and other diagnostic imaging

- preventive services

However, the services must meet the criteria of being medically necessary and align with accepted standards of medical practice.

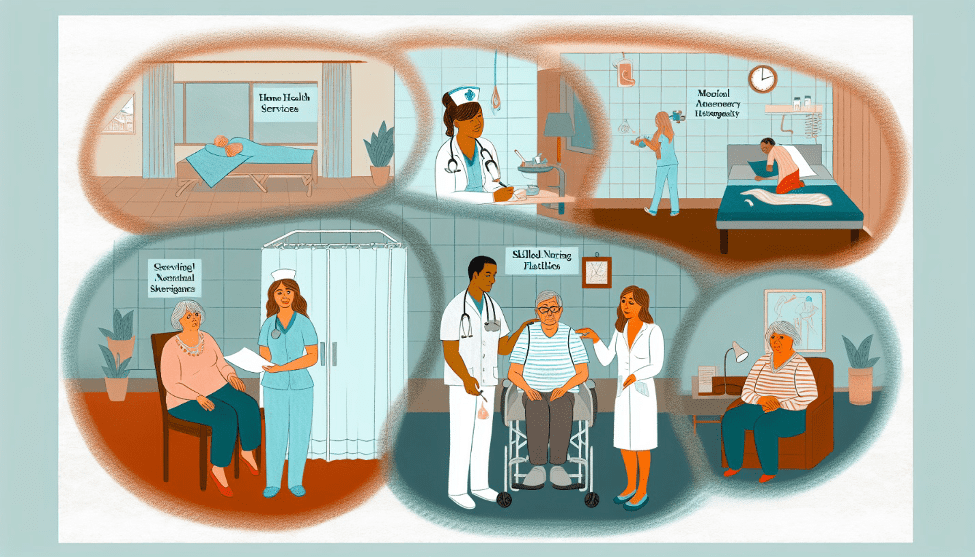

Home Health Services

When health issues confine you to your home, it may be challenging to access the medical services you need. That’s where Medicare Part B could step in, possibly providing coverage for specific home health services, which may include skilled nursing services, skilled therapy, and care administered by a home health aide.

These services could be provided on a part-time or intermittent basis, possibly allowing up to 8 hours a day and no more than 28 hours per week.

Mental Health Care

Mental health is just as important as physical health, and Medicare Part B will likely recognize this. Part B may also provide coverage for outpatient mental health services, such as individual and group psychotherapy conducted by licensed professionals.

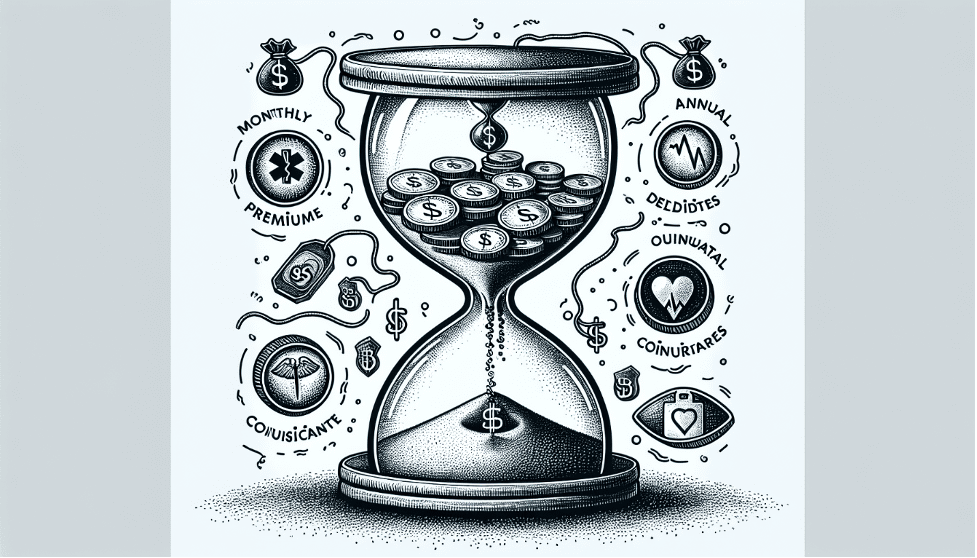

Potential Medicare Part B Costs and Premiums

While Medicare Part B might come with some associated costs, understanding them may be crucial for effective healthcare budget planning.

Coinsurance and Out-of-Pocket Costs

Once the annual deductible has been met, beneficiaries may be required to cover up to a 20% coinsurance with certain Medicare Part B services. However, some preventive care services covered by Medicare Part B might not necessitate a coinsurance fee.

What Medicare Part B Does Not Cover

While Medicare Part B could provide comprehensive coverage, it may not cover certain services.

Cosmetic Surgery

While Medicare Part B could cover a wide array of medical services, it may not cover cosmetic surgery unless it has been deemed medically necessary.

This means if you’re planning to get a nose job or facelift, Medicare Part B might not cover it unless it’s necessary due to accidental injury or to improve the function of a malformed body part.

Routine Eye Exams

If you’re thinking of getting a routine eye exam for eyeglasses or contact lenses, Medicare Part B may not cover this service.

However, it could offer coverage for certain tests and treatment for eye diseases and conditions if you have age-related macular degeneration, diabetes, or are at risk for glaucoma.

Medicare Advantage Plans and Supplement Insurance

For those who might need more coverage than what Original Medicare offers, there will likely be additional coverage options available, such as the Medicare Advantage (Part C) and Medicare Supplement Insurance.

Medicare Advantage (Part C)

Medicare Advantage plans, also known as Medicare Part C, offer the same benefits as Original Medicare but may also provide additional coverage such as a Medicare drug plan, dental coverage, and vision coverage.

However, these plans, offered by private insurance companies, may have different rules and coverage restrictions and may require an extra monthly premium.

Medicare Supplement Insurance

Medicare Supplement Insurance, also known as Medigap, could be purchased from a private health insurance company to potentially help cover the costs that Original Medicare might not cover, such as copayments, coinsurance, and deductibles. However, these plans cannot be held simultaneously with a Medicare Advantage plan.

Navigating Medicare Enrollment and Choices

Understanding the ins and outs of Medicare is just the first step. Understanding the intricacies of enrollment periods and comparing different plans could be key to making informed healthcare coverage decisions.

Enrollment Periods

There are specific enrollment periods for Medicare, including the Initial Enrollment Period, General Enrollment Period, and Special Enrollment Period. Failing to enroll within the specified period may incur a penalty, so awareness of these periods may be vital to potentially avoid extra costs.

To enroll, call one of our licensed agents at 1-833-641-4938 (TTY 711), Mon-Fri 8 am-9 pm EST. They can provide comprehensive information, personalized guidance, and ongoing assistance to navigate the enrollment process for private insurance companies, making it easier for beneficiaries to make informed decisions about their healthcare.

Comparing Plans

Selecting a Medicare plan is a highly individualized process. Comparing Medicare Advantage and Medicare Supplement Insurance plans could be crucial for finding the most suitable coverage for your needs. Each plan will likely offer different benefits and costs, so you may want to consider your potential healthcare needs and budget when comparing plans.

Summary

This article has helped you understand Medicare Part B’s potential coverage, costs, and the services it might not cover. This article has also explored the additional coverage options through certain Medicare Advantage and Medicare Supplement Insurance plans and learned about the importance of understanding enrollment periods and comparing plans.

Knowledge is power, and with this newfound understanding of Medicare Part B, you’re now equipped to take control of your healthcare decisions.

Frequently Asked Questions

→ What is covered in Part B of Medicare?

Medicare Part B will likely cover most doctor visits, outpatient medical services, durable medical equipment, and preventive services like vaccines and wellness exams. It may also pay for medical necessities and preventive services like exams, lab tests, and screening shots to help prevent, find, or manage medical problems.

→ What is Medicare Part C used for?

Medicare Part C, also known as Medicare Advantage, will likely be used for providing coverage for inpatient care such as hospital stays, skilled nursing facility care, hospice care, home health care, and care in religious non-medical health care institutions. Some plans may also offer additional benefits beyond Original Medicare.

→ How do I compare different Medicare plans?

When comparing Medicare plans, you may want to consider the additional benefits, coverage for out-of-pocket expenses, prescription drug coverage, overall costs, and provider network restrictions, based on your personal healthcare needs and preferences.

ZRN Health & Financial Services, LLC, a Texas limited liability company

Russell Noga is the CEO of ZRN Health & Financial Services, and head content editor of several Medicare insurance online publications. He has over 15 years of experience as a licensed Medicare insurance broker helping Medicare beneficiaries learn about Medicare, Medicare Advantage Plans, Medigap insurance, and Medicare Part D prescription drug plans.