UHC Medicare Advantage Plans 2026

Wondering how UHC Medicare Advantage Plans

Key Takeaways

- UnitedHealthcare Medicare Advantage Plans combine Original Medicare benefits with additional services like dental, vision, and wellness programs.

- In 2025, UHC will introduce 140 new Medicare Advantage plans, enhancing flexibility and accessibility for members, including $0 copays for many services.

- Eligibility for these plans requires enrollment in Original Medicare, with specific plans available for dual-eligible individuals and those with chronic conditions.

Compare Plans in One Step!

Enter Zip Code

Understanding UHC Medicare Advantage Plans 2026

UnitedHealthcare Medicare Advantage Plans are designed to combine the benefits of hospital and medical insurance from Original Medicare into a single, comprehensive plan. Unlike Original Medicare, which is directly provided by the federal government, these plans are offered through private insurance companies like UnitedHealthcare. This structure allows for the inclusion of additional benefits that enhance the overall healthcare experience.

Eligibility for these plans generally requires individuals to be enrolled in Original Medicare. Additional services often included in these plans are dental, vision, and wellness programs, frequently at no extra premium. Geographic location plays a significant role in determining coverage and costs, as Medicare Advantage Plans operate within defined areas, ensuring that beneficiaries receive tailored care based on their location.

Types of UHC Medicare Advantage Plans Available 2026

UnitedHealthcare offers a variety of Medicare Advantage Plans to cater to different healthcare needs. These include Health Maintenance Organization (HMO) plans, Preferred Provider Organization (PPO) plans, and Special Needs Plans (SNPs). Each type of plan has its unique features and benefits, providing options that can suit a wide range of individual preferences and requirements.

HMO Plans

HMO plans from UnitedHealthcare require members to choose a primary care physician (PCP) who will coordinate all their healthcare needs. Typically, these plans have low or no monthly premiums, making them an attractive option for those looking to minimize their healthcare costs. However, it’s important to note that HMO plans generally do not cover out-of-network services except in emergencies, which emphasizes the importance of staying within the provider network.

In 2025, UnitedHealthcare will introduce 140 new HMO plans, increasing access and options for consumers. Members will enjoy benefits such as $0 copays for preventive care, lab tests, and virtual visits. Additional perks might include credits for over-the-counter products and healthy food, enhancing the overall value of these plans.

PPO Plans

PPO plans offered by UnitedHealthcare provide greater flexibility compared to HMO plans. Members can see any doctor who accepts Medicare, without the need for referrals, making it easier to access the care they need. This flexibility extends to out-of-network providers, although staying in-network typically results in lower costs.

In 2025, UnitedHealthcare will expand its PPO offerings with 140 new plans to meet diverse consumer needs. Benefits will include $0 copay for virtual medical visits, preventive services, and certain prescription drugs. With access to a national provider network of over 1 million healthcare providers, members can be assured of broad access to care.

Special Needs Plans (SNPs)

Special Needs Plans (SNPs) are tailored Medicare Advantage plans designed to meet the unique needs of specific populations. There are three main types of SNPs: Dual Special Needs Plans (d snp) for individuals eligible for both Medicare and Medicaid, Chronic Special Needs Plans (C-SNPs) for those with serious chronic conditions, and Institutional Special Needs Plans (I-SNPs) for residents of skilled nursing facilities.

These plans offer targeted healthcare support and include prescription drug coverage as part of their benefits. D-SNPs, for instance, provide additional assistance in coordinating Medicare and Medicaid benefits, while C-SNPs focus on managing chronic conditions such as diabetes and heart failure. I-SNPs cater to individuals needing extensive care in nursing facilities, ensuring they receive the specialized care they require.

Overview of UHC Medicare Advantage Plans 2026

UnitedHealthcare is set to introduce 140 new Medicare Advantage plans in 2025, expanding its offerings to meet the diverse needs of consumers. The goal is to maintain coverage for 96% of Medicare consumers, ensuring that a wide range of needs are met through these enhanced plans.

A significant expansion includes the Dual Special Needs Plans, which will reach an additional 135,000 dual-eligible consumers. Members will benefit from $0 copays for certain preventive services, including annual physical exams and lab tests, and will be incentivized through a new rewards program that encourages health-related activities such as wellness visits.

Furthermore, the UCard will be upgraded to a more secure magstripe technology, simplifying access to benefits. The Medicare Advantage formulary will cover more frequently used tier 1 prescriptions compared to competitors, adding another layer of value for members.

Covered Services and Benefits

All Medicare Advantage plans offered by UnitedHealthcare encompass the benefits of Medicare Part A (hospital insurance) and Part B (medical insurance), often including additional services not covered by Original Medicare. This comprehensive coverage frequently includes prescription drug plans, enhancing the overall healthcare experience for members.

Additional services commonly offered by these plans include dental care, vision exams, and fitness memberships, often at no extra premium. Some plans may also provide transportation services for medical appointments and virtual healthcare visits, making healthcare more accessible.

However, it’s important to note that hospice care remains funded by Original Medicare Part A.

Key Benefits of UHC Medicare Advantage Plans

UnitedHealthcare’s new plans for 2025 include 140 new options designed to cater to varying consumer needs. Most plans will offer $0 copays for annual physical exams, lab tests, and preventive care, making essential healthcare services more accessible.

Members will also benefit from access to a vast provider network covering nearly 96% of Medicare-eligible individuals in the service area. New benefits for dual-eligible consumers will include credits for over-the-counter products and healthy food, adding value to these plans.

The Chronic Special Needs Plans (C-SNPs) will nearly double in availability, covering 70% of individuals with severe chronic conditions. Additionally, a new rewards program will incentivize healthy activities like annual wellness visits, and the UCard will transition to magstripe technology, enhancing usability for members in managing their benefits.

Additional Health Services

UnitedHealthcare Medicare Advantage Plans often include additional health services such as dental, vision, and wellness programs at no extra cost. These services can significantly enhance the overall healthcare experience for members. For instance, certain plans offer transportation to medical appointments, making it easier for members to access necessary care.

Virtual provider visits are also commonly included, enhancing accessibility and convenience. Wellness programs focusing on preventive care, such as fitness memberships and physical activity, are another valuable addition.

UnitedHealthcare also offers wellness and rewards programs designed to encourage healthy lifestyles and potentially provide financial incentives for achieving health-related goals. Supplemental services such as dental, vision, and hearing coverage are often available, providing comprehensive care for members.

Furthermore, managing chronic conditions and mental health services can affect key aspects of maintaining overall health.

Enrollment Process for UHC Medicare Advantage Plans

The enrollment process for UnitedHealthcare Medicare Advantage Plans is structured to ensure that beneficiaries can easily navigate their options and select the plan that best fits their needs. Enrollment in these plans is dependent on the renewal of the plan’s contract with Medicare each year, making it essential for beneficiaries to stay informed about their options.

When to Enroll

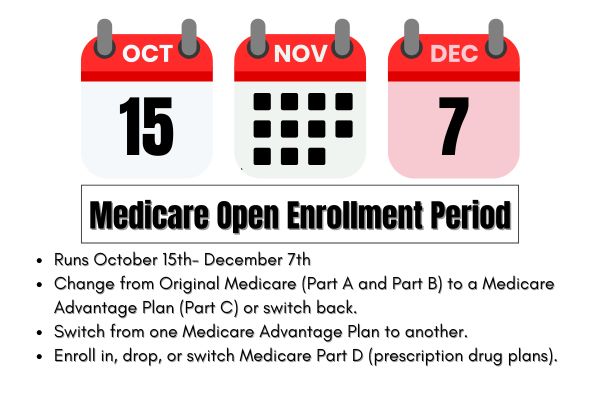

The Annual Enrollment Period (AEP) for Medicare runs from October 15 to December 7 each year. During this time, beneficiaries can enroll in UHC Medicare Advantage Plans, making any necessary changes to their coverage for the upcoming year. Additionally, individuals can start enrolling in new UHC Medicare Advantage options as early as October 1, 2024, for the following year.

The Initial Enrollment Period (IEP) for newcomers to Medicare starts three months before and ends three months after their 65th birthday. Current Medicare beneficiaries wishing to change plans can do so during the Medicare Advantage Open Enrollment Period (MA OEP) from January 1 to March 31 each year.

Special Enrollment Periods (SEPs) can also arise from specific life events, providing additional opportunities to enroll or make changes to coverage.

Different enrollment periods

There are multiple enrollment periods for Medicare beneficiaries, each catering to different situations. The Initial Enrollment Period (IEP) is for new beneficiaries and lasts seven months, beginning three months before turning 65 and concluding three months after the birthday month.

The General Enrollment Period (GEP) occurs annually from January 1 to March 31, allowing individuals to sign up for Medicare coverage if they missed their IEP.

Special Enrollment Periods (SEPs) allow individuals to enroll in Medicare without penalty under certain circumstances, such as losing other health coverage. Coverage typically begins the month after enrollment during the GEP.

OEP, AEP, Special Enrollment

The Open Enrollment Period (OEP) allows existing Medicare members to make changes to their Medicare Advantage plans or switch back to Original Medicare from January 1 to March 31 each year. This period provides a crucial opportunity for those who may want to adjust their coverage based on new healthcare needs or changes in plan benefits.

The Annual Enrollment Period (AEP) occurs from October 15 to December 7 each calendar year, enabling beneficiaries to modify their plans for the upcoming year.

Special Enrollment Periods (SEPs) are available for individuals experiencing qualifying life events, such as relocation or changes in health status, allowing them to change their Medicare plans outside of the standard enrollment periods. These periods ensure that beneficiaries have multiple opportunities throughout the year to secure the best possible coverage for their needs.

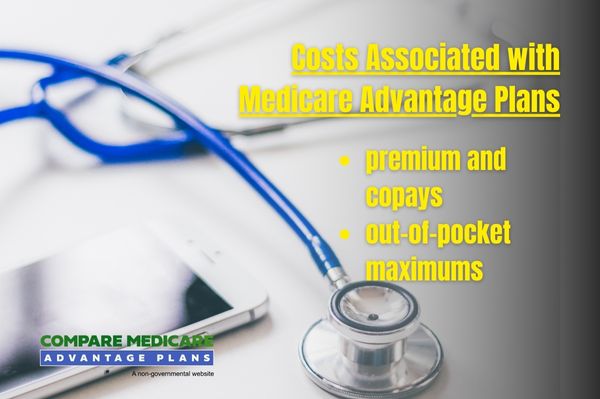

Costs Associated with UHC Medicare Advantage Plans

The costs associated with UnitedHealthcare Medicare Advantage Plans can vary significantly depending on the specific plan and the services covered. These plans often feature $0 premiums and copays for primary care visits and preventive services, making them financially accessible for many members.

Understanding the cost structure, including premiums, copays, and out-of-pocket maximums, is essential for beneficiaries to effectively manage their healthcare expenses.

Premiums and Co-Pays

UnitedHealthcare Medicare Advantage plans typically include an annual deductible and various copays for covered services. Many plans include $0 copays for primary care visits and preventive services, allowing members to access essential healthcare without worrying about out-of-pocket costs. Stability in copay amounts for specialist visits and prescription drugs is another benefit, making it easier for members to budget for their healthcare expenses.

In addition to $0 premiums for many plans, UnitedHealthcare offers monthly credits to help offset out-of-pocket costs for Medicare-covered services. This financial support can be particularly beneficial for members managing chronic conditions or requiring frequent medical care. For 2025, many plans will also offer $0 copays for routine services, including primary care visits and preventive care. Chronic Special Needs Plans (C-SNPs) will feature lower average copays for essential healthcare services, further enhancing affordability.

Out-of-Pocket Maximums

Each Medicare Advantage plan has a defined out-of-pocket maximum, limiting the total annual expenses members must cover. This cap provides significant financial protection by ensuring that there is a maximum limit on how much a member will spend on covered services in a given year. UnitedHealthcare’s plans for 2025 feature lower out-of-pocket maximums, making it easier for members to manage their healthcare costs.

For the year 2025, the out-of-pocket maximum (OOPM) for individual plans is set at $9,200, while for family plans, it is $18,400, reflecting a 2.6% decrease compared to 2024. This cap encompasses all copayments, deductibles, and coinsurance for both medical and pharmacy benefits within the plan year.

The OOPM is adjusted annually by the Department of Health and Human Services (HHS) and applies to most group health plans.

Covered Services and Benefits

UnitedHealthcare Medicare Advantage plans encompass all the benefits of Original Medicare, including hospital and doctor visits, and often include prescription drug coverage. Many of these plans feature $0 monthly premiums, enabling cost-effective access to necessary health services. Preventive care like annual physical exams, lab tests, and screenings are typically provided at no cost under UHC Medicare Advantage plans, ensuring members can maintain their health without incurring additional expenses.

In addition to standard benefits, members may also enjoy $0 copays for dental, vision, and hearing exams. Dental services cover both preventive and comprehensive treatments, such as cleanings and root canals, while vision benefits often include allowances for eyewear and free eye exams.

Hearing benefits may include routine hearing exams at no charge and discounts on hearing aids. Members can also benefit from rewards for completing healthy activities, such as annual wellness visits.

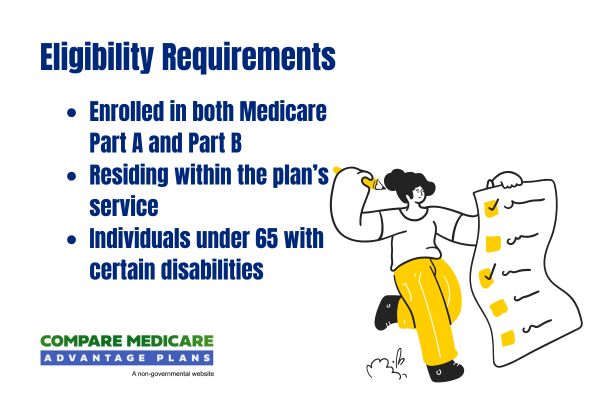

How to Qualify for UHC Medicare Advantage Plans

Eligibility for UnitedHealthcare Medicare Advantage Plans generally requires individuals to be enrolled in Medicare Parts A and B. Additionally, certain plans cater specifically to dual-eligible individuals, providing extra benefits for those who qualify for both Medicare and Medicaid. Eligibility for some Special Needs Plans requires meeting specific health criteria related to chronic conditions.

Geographic availability is another factor to consider, as plan eligibility may vary based on location. Prospective members should review UnitedHealthcare plan details or consult their representatives to understand the qualification criteria fully. Residents in areas where UHC operates can find tailored plans that suit their healthcare needs.

Contracted Network and Access to Care

UnitedHealthcare provides access to a vast national provider network that covers nearly 96% of individuals eligible for Medicare within its service areas. Members can utilize a network of over 1 million healthcare providers, ensuring they have options both locally and while traveling. The enhanced provider search function helps members locate appropriate care more easily, adding to the convenience.

The Medicare Advantage formulary from UnitedHealthcare maintains extensive coverage for frequently prescribed medications, especially for those managing chronic health conditions. Members benefit from a streamlined all-in-one access card called the UCard, which simplifies the process of utilizing various health services. This comprehensive network and streamlined access ensure that members receive the care they need when they need it.

Comparing UHC Medicare Advantage Plans to Original Medicare

Comparing UHC Medicare Advantage Plans to Original Medicare reveals significant differences in benefits and costs. More than half of eligible Medicare beneficiaries are opting for Medicare Advantage plans over Original Medicare, primarily due to the additional benefits and financial protections these plans offer.

Coverage Differences

Medicare Advantage plans often provide additional benefits not covered by Original Medicare, such as vision, dental, and fitness programs. While Original Medicare consists of Part A and Part B, Medicare Advantage combines these into one plan, frequently including prescription drug coverage. Unlike Original Medicare, which has no annual out-of-pocket maximum, Medicare Advantage plans impose a cap on annual out-of-pocket expenses, limited to $9,350 in-network for 2025.

Original Medicare is provided directly by the federal government, while Medicare Advantage plans are offered through private insurance companies that contract with the government. These plans often include coverage for prescription drugs, which are not covered under Original Medicare unless a separate Part D plan is purchased.

Medicare Advantage plans combine coverage for hospital and provider visits into a single plan, often including additional benefits not found in Original Medicare.

Cost Comparisons

While Original Medicare typically charges a standard premium for Part B, many Medicare Advantage plans offer $0 premium options along with predictable copays. Most Medicare Advantage plans have a $0 premium option, contrasting with Original Medicare, which has standard premiums and deductibles. These plans also impose an annual out-of-pocket maximum, capping expenses at no more than $9,350 for in-network services in 2025.

Medicare Advantage plans provide significant financial protection by limiting out-of-pocket expenses annually, which is a considerable advantage compared to Original Medicare. While Original Medicare typically covers about 80% of healthcare costs, Medicare Advantage plans offer predictable copays and coinsurance, potentially reducing unexpected expenses.

Choosing between UHC Medicare Advantage and Original Medicare often hinges on cost, as Advantage plans typically feature low or no monthly premiums.

Emergencies and Referrals

In UHC Medicare Advantage plans, emergency services are covered regardless of the provider network, ensuring that members receive necessary treatment without needing prior authorization. This flexibility is crucial in urgent situations where immediate care is required. Members can access care from any doctor or hospital during emergencies, but it is important to notify their network provider as soon as possible.

For non-emergency referrals, UnitedHealthcare typically requires members with HMO plans to consult their primary care physician to get authorized access to specialists. However, members of PPO plans do not require a referral to see a specialist, providing greater flexibility in accessing care.

Having the UnitedHealthcare card on hand during emergencies can streamline the care process, ensuring that members receive timely and appropriate treatment.

Summary

In summary, UnitedHealthcare Medicare Advantage Plans

Frequently Asked Questions

→ What are the main differences between UHC Medicare Advantage Plans and Original Medicare?

UHC Medicare Advantage Plans offer a bundled approach that includes hospital and medical insurance along with additional benefits such as vision, dental, and prescription drug coverage, which Original Medicare does not provide. This integrated coverage can enhance your healthcare experience significantly.

→ When can I enroll in a UHC Medicare Advantage Plan?

You can enroll in a UHC Medicare Advantage Plan during the Annual Enrollment Period from October 15 to December 7, the Medicare Advantage Open Enrollment Period from January 1 to March 31, or during Special Enrollment Periods due to qualifying life events. Make sure to check your eligibility during these times to ensure you have the coverage you need.

→ What costs are associated with UHC Medicare Advantage Plans?

UHC Medicare Advantage Plans typically involve costs such as premiums, copays, and deductibles, though many plans feature $0 premiums and copays for primary care visits and preventive services. Out-of-pocket maximums are also in place to help limit your annual expenses.

→ What additional health services are included in UHC Medicare Advantage Plans?

UHC Medicare Advantage Plans typically include additional health services such as dental, vision, and hearing exams, wellness programs, transportation to medical appointments, and virtual provider visits. These enhancements aim to provide comprehensive care for enrollees.

→ How do I qualify for a UHC Medicare Advantage Plan?

To qualify for a UHC Medicare Advantage Plan, you must be enrolled in Medicare Parts A and B. Additional criteria may apply for specific plans, such as health conditions or dual eligibility for Medicare and Medicaid.

ZRN Health & Financial Services, LLC, a Texas limited liability company

Russell Noga is the CEO of ZRN Health & Financial Services, and head content editor of several Medicare insurance online publications. He has over 15 years of experience as a licensed Medicare insurance broker helping Medicare beneficiaries learn about Medicare, Medicare Advantage Plans, Medigap insurance, and Medicare Part D prescription drug plans.